Understanding Debt Settlement in New Jersey

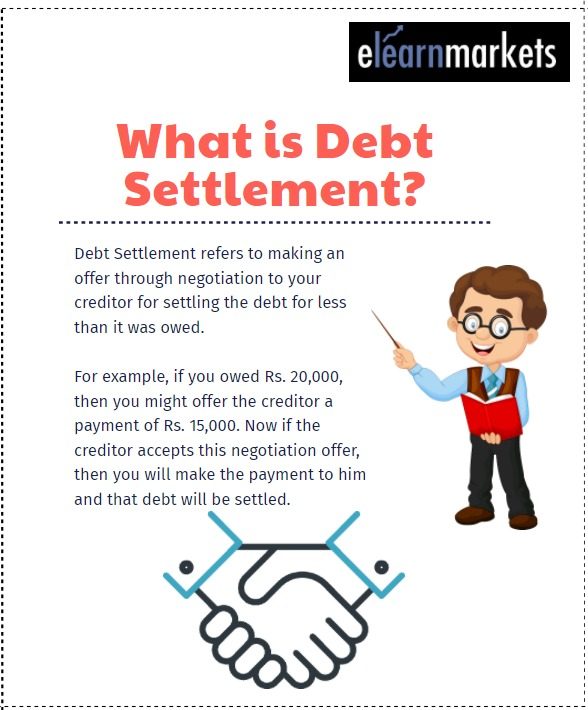

If you’re struggling with overwhelming debt, debt settlement in New Jersey may be a lifesaver. It’s a legal process that allows you to negotiate with your creditors to pay less than what you owe. This can be a great way to get out of debt for good and rebuild your credit score. However, it’s important to understand the process before you get started. You’ll need to find a reputable debt settlement company to work with, and you’ll need to be prepared to make some sacrifices in order to get the best possible deal. But if you’re willing to put in the work, debt settlement can be a great way to get back on your feet financially.

There are several different types of debt that can be settled, including credit card debt, medical debt, and personal loans. However, not all debts are eligible for settlement. For example, student loans and taxes are typically not eligible. If you’re not sure whether or not your debt is eligible for settlement, you can contact a debt settlement company for a free consultation.

The debt settlement process typically takes several months to complete. During this time, you’ll make monthly payments to your debt settlement company. The company will then use this money to negotiate with your creditors on your behalf. Once a settlement is reached, you’ll make a final payment to your debt settlement company, and your debt will be considered paid in full.

Debt settlement can have a negative impact on your credit score. However, the impact will be less severe than if you file for bankruptcy. If you’re considering debt settlement, it’s important to weigh the pros and cons carefully to make sure it’s the right decision for you.

Debt Settlement in New Jersey: A Lifeline for the Financially Burdened

Are you drowning in a sea of debt, struggling to keep your head above water? Debt settlement can be your beacon of hope, guiding you towards financial salvation. This debt relief strategy offers a glimmer of hope for New Jersey residents eager to break free from the clutches of overwhelming obligations.

Benefits of Debt Settlement

Debt settlement is an invaluable tool for those who are struggling to repay their debts. It offers a wealth of benefits that can transform your financial situation:

Reduced Debt Balances

The primary allure of debt settlement is its ability to significantly reduce your debt balances. By negotiating with creditors, you can potentially lower your total debt by 50% or more, freeing up a substantial portion of your income for other essential expenses.

Improved Cash Flow

With reduced debt payments, you’ll have more money to allocate towards other priorities. This improved cash flow can ease the financial strain, allowing you to make ends meet, save for the future, and enjoy a peace of mind that has long eluded you.

Enhanced Credit Score

While debt settlement can temporarily impact your credit score, the long-term effects can be positive. By successfully completing a settlement, you’ll eliminate the burden of high-interest debts and missed payments, which can boost your score over time.

Peace of Mind

Financial stress can take a heavy toll on your well-being. Debt settlement offers a ray of hope, reducing anxiety and providing a sense of control over your financial future. You’ll no longer have to endure the relentless phone calls and letters from creditors, giving you the space to breathe and focus on rebuilding your financial stability.

Easier Credit Access

Once your debts are settled, you’ll be more likely to qualify for loans and credit cards with favorable terms. Lenders will see that you’ve taken steps to address your financial challenges, increasing your chances of approval and securing lower interest rates.

Debt Settlement in New Jersey: Weigh the Pros and Cons

Debt settlement can be a tempting option for those struggling with overwhelming debt in New Jersey. However, it’s crucial to understand the potential drawbacks before taking this route. Debt settlement can have serious consequences, including a damaged credit score, tax implications, and a prolonged period of rebuilding financial stability.

Disadvantages of Debt Settlement

1. Damaged Credit Score

Debt settlement companies often negotiate with creditors to pay less than the full amount owed. While this can reduce the overall debt amount, it negatively impacts your credit score. The settlement will be recorded on your credit report, which can lower your score significantly.

This can make it difficult to obtain new credit or loans in the future, and it can also result in higher interest rates.

2. Tax Implications

The IRS considers forgiven debt as taxable income. When you settle a debt for less than the amount owed, the difference is treated as income. This can result in a hefty tax bill, especially for large amounts of settled debt.

3. Prolonged Period of Financial Recovery

Debt settlement can take several months or even years to complete. During this time, you may have to make regular payments to the settlement company. These payments can be a significant financial burden, especially if you’re already struggling with debt.

Additionally, the negative impact on your credit score can make it difficult to rebuild your financial situation quickly.

4. Impact on Co-Signers

If you have a co-signer on any of your debts, debt settlement can also affect their credit score. When you settle a debt, the co-signer is still legally responsible for the full amount owed.

This means that if you default on the settlement, the co-signer could be sued by the creditor.

5. Potential Legal Issues

Working with debt settlement companies can be risky. Some companies may use unethical or illegal practices, such as charging excessive fees or misrepresenting the terms of the settlement. It’s important to choose a reputable company and to carefully review all the terms before signing any contracts.

Debt Settlement in New Jersey: A Guide

Are you struggling to pay off your debts? Feeling overwhelmed by the constant pressure of collectors calling and letters piling up? Debt settlement in New Jersey could be an option for you. This process involves negotiating with your creditors to pay less than the full amount you owe, potentially offering a way out of the financial burden that’s weighing you down.

How Debt Settlement Works

Debt settlement companies work on your behalf to negotiate with creditors and reduce your debt obligations. They typically charge a fee for their services, and the process can take several months or even years to complete. It’s important to note that debt settlement can have a negative impact on your credit score, and it may not be the best option for everyone.

Alternatives to Debt Settlement

There are other options available to debtors who are struggling with debt, such as bankruptcy and debt management plans. Bankruptcy is a legal proceeding that discharges your debts, but it also has serious consequences, including a negative impact on your credit score and the potential loss of assets.

Debt Management Plans

Debt management plans are offered by non-profit credit counseling agencies and involve consolidating your debts into a single monthly payment. This can make it easier to manage your debt and reduce the amount of interest you pay, but it doesn’t eliminate your debt entirely.

Debt Consolidation Loans

Debt consolidation loans allow you to combine multiple debts into a single loan with a lower interest rate. This can simplify your monthly payments and potentially save you money on interest. However, you’ll still need to pay off the full amount you owe, and qualifying for a debt consolidation loan can be difficult if you have bad credit.

Credit Counseling

Credit counseling agencies offer free or low-cost services to help you manage your debt and improve your financial situation. They can provide guidance on budgeting, debt management, and credit repair. Credit counseling can be a valuable resource for anyone struggling with debt, regardless of whether they choose to pursue debt settlement.

**Debt Settlement in New Jersey: A Guide to Getting Out of Debt**

If you’re struggling with overwhelming debt, debt settlement may be a viable option for you. In New Jersey, several reputable companies offer debt settlement services to help you negotiate with creditors and consolidate your debt into a single, lower monthly payment. However, before you embark on this journey, it’s crucial to understand the process, choose a reputable company, and prepare for the potential consequences.

Understanding Debt Settlement

Debt settlement is a process where you negotiate with your creditors to pay back less than the full amount you owe. This can be a tempting solution if you’re unable to make the minimum payments on your debt or if you’re facing foreclosure or bankruptcy. However, it’s important to note that debt settlement can have a negative impact on your credit score and may result in tax consequences.

Choosing a Debt Settlement Company

If you decide to pursue debt settlement, it is important to choose a reputable company that has experience and a good track record. There are several factors to consider when selecting a company, including:

* **Fees:** Debt settlement companies typically charge a monthly fee or a percentage of the amount you settle for. Understand the fee structure before committing to a company.

* **Experience:** Choose a company that has been in business for several years and has a proven track record of success.

* **Negotiation skills:** Look for a company with experienced negotiators who can effectively communicate with creditors on your behalf.

* **Communication:** Choose a company that provides clear and regular communication throughout the process.

* **Customer service:** Select a company that values customer service and is responsive to your needs.

**Preparing for Debt Settlement**

Before enrolling in a debt settlement program, it’s essential to be prepared for the potential consequences:

* **Credit score:** Debt settlement can negatively impact your credit score, making it difficult to qualify for loans or other financial products in the future.

* **Tax consequences:** In some cases, the amount forgiven by creditors may be considered taxable income. Consult with a tax professional to understand the potential tax implications.

* **Lawsuits:** If you default on your debt settlement program or violate the terms of your agreement, creditors may sue you for the full amount you owe.

**Alternatives to Debt Settlement**

If you’re considering debt settlement, it’s worth exploring alternative options:

* **Debt consolidation:** Combine multiple debts into a single, lower-interest loan.

* **Credit counseling:** Seek guidance from a non-profit credit counselor to create a budget and manage debt.

* **Bankruptcy:** In extreme cases, bankruptcy may be a last resort option, but it comes with significant consequences.

**Conclusion**

Debt settlement can be a challenging but potentially rewarding option for individuals facing overwhelming debt. By understanding the process, choosing a reputable company, and preparing for the potential consequences, you can increase your chances of successfully resolving your debt issues. However, it’s important to remember that debt settlement is not a quick fix. It requires time, patience, and a commitment to financial responsibility.

No responses yet