Debt Settlement NJ: A Comprehensive Guide

In the bustling state of New Jersey, individuals grappling with overwhelming debt often turn to debt settlement as a lifeline. This financial solution aims to ease the burden by negotiating with creditors to reduce the balance owed. While it may seem like a tempting prospect, it’s essential to fully understand the process, benefits, and potential drawbacks involved.

Process of Debt Settlement

Debt settlement companies serve as intermediaries between debtors and creditors. They typically initiate negotiations with creditors on behalf of the debtor, aiming to reduce the total amount owed. This involves a process of back-and-forth communication, where the debt settlement company argues for a lower payment amount based on the debtor’s financial situation. If the creditor agrees, the debtor makes a lump sum payment that settles the debt for a reduced amount.

Advantages of Debt Settlement

One of the primary advantages of debt settlement is the potential for significant debt reduction. Debtors can often settle their debts for 50% or less of the original balance. Additionally, debt settlement can pause collection activities and improve a debtor’s credit score over time.

Disadvantages of Debt Settlement

Despite its potential benefits, debt settlement also comes with certain risks. One major concern is the negative impact on credit scores. The settlement process typically involves defaulting on payments, which can lead to a significant drop in credit ratings. Moreover, debt settlement companies may charge high fees, which can further strain a debtor’s finances.

Eligibility for Debt Settlement

Not everyone qualifies for debt settlement. Generally, individuals with high levels of unsecured debt and a low ability to repay their debts are considered suitable candidates. Debt settlement companies typically require debtors to have a debt-to-income ratio of over 50% and a FICO score below 640.

Tips for Choosing a Debt Settlement Company

If you’re considering debt settlement, it’s crucial to choose a reputable and experienced company. Look for companies with a proven track record of success and positive customer reviews. Avoid companies that make unrealistic promises or charge upfront fees.

Debt Settlement NJ: A Path to Financial Freedom

Are you drowning in a sea of debt, feeling like there’s no way out? Debt settlement might be your lifeline. However, it’s not a magic wand that will solve all your financial woes. Let’s dive into the nitty-gritty and explore who qualifies for this life-changing opportunity.

Eligibility

Not all roads lead to debt settlement. It’s typically reserved for those who have accumulated a significant amount of unsecured debt, such as credit cards and personal loans. Moreover, your income should be low enough that making full payments on your debt is an insurmountable challenge. In short, if you’re feeling overwhelmed and can’t seem to catch a break, debt settlement could be the solution you’ve been searching for.

1. Unsecured Debt

What kind of debt do you owe? If it’s unsecured, meaning it isn’t backed by any collateral, you may be eligible for debt settlement. Common forms include credit card balances, medical bills, and payday loans.

2. Income Limitations

Your income plays a crucial role in determining your eligibility. Debt settlement programs typically have income limits in place to ensure that you can afford to make the monthly payments required to settle your debt over a period of time.

3. High Debt-to-Income Ratio

This ratio measures how much of your monthly income goes towards paying off debt. If you’re struggling to keep up with your debt payments and a significant portion of your income is already being eaten up, you may qualify for debt settlement.

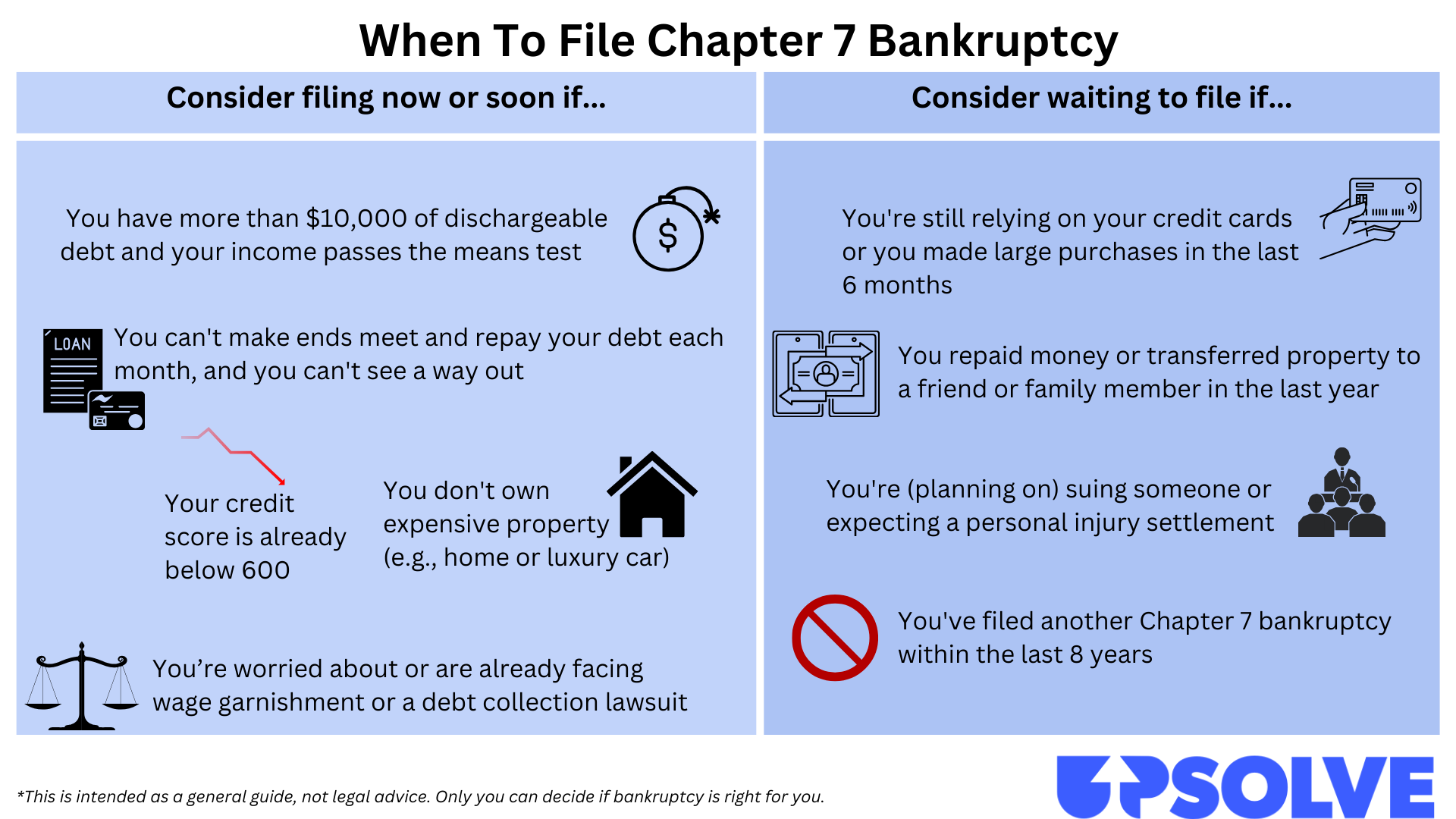

4. No Recent Bankruptcies

If you’ve filed for bankruptcy in the past, you may not be eligible for debt settlement. This is because bankruptcy already provides a legal mechanism for resolving debts.

5. Understanding the Process

Debt settlement isn’t a quick fix. It requires patience, persistence, and a commitment to making regular payments. The process typically involves negotiating with creditors to reduce your debt balance. However, it’s important to note that debt settlement can have a negative impact on your credit score. Weigh the pros and cons carefully before making a decision.

Debt Settlement NJ: A Guide to Getting Out of Debt

If you’re struggling with debt, you’re not alone. Millions of Americans are in the same boat. And while there’s no one-size-fits-all solution, debt settlement could be a good option for you. Debt settlement is a process of negotiating with your creditors to pay less than the full amount you owe. This can be a great way to get out of debt faster and save money on interest.

How Does Debt Settlement Work?

Debt settlement companies work with you to negotiate with your creditors on your behalf. They’ll typically charge a fee for their services, but they can often save you thousands of dollars in the long run. The process of debt settlement can take several months or even years, but it can be worth it if you’re able to significantly reduce your debt.

Is Debt Settlement Right for You?

Debt settlement is not right for everyone. If you’re considering debt settlement, it’s important to weigh the pros and cons carefully. Here are some things to consider:

- The impact on your credit score. Debt settlement can have a negative impact on your credit score. This is because it’s considered a form of defaulting on your debt.

- The potential for tax consequences. The money you save through debt settlement may be considered taxable income. This means you could owe taxes on the amount you save.

- The time and effort involved. Debt settlement can be a long and complex process. It’s important to be prepared to commit to the process if you want to be successful.

Alternatives to Debt Settlement

If you’re not sure if debt settlement is right for you, there are other options for managing debt. These include:

Credit Counseling

Credit counseling is a free or low-cost service that can help you create a budget, manage your debt, and improve your credit score. Credit counselors can also help you negotiate with your creditors on your own behalf.

Debt Consolidation Loans

Debt consolidation loans allow you to combine multiple debts into a single loan with a lower interest rate. This can make it easier to manage your debt and pay it off faster.

Bankruptcy

Bankruptcy is a legal proceeding that allows you to discharge your debts. This can be a last resort, but it can be a good option if you’re unable to repay your debts.

Which Option Is Right for You?

The best option for managing debt depends on your individual circumstances. If you’re not sure which option is right for you, it’s a good idea to talk to a credit counselor or financial advisor.

No responses yet