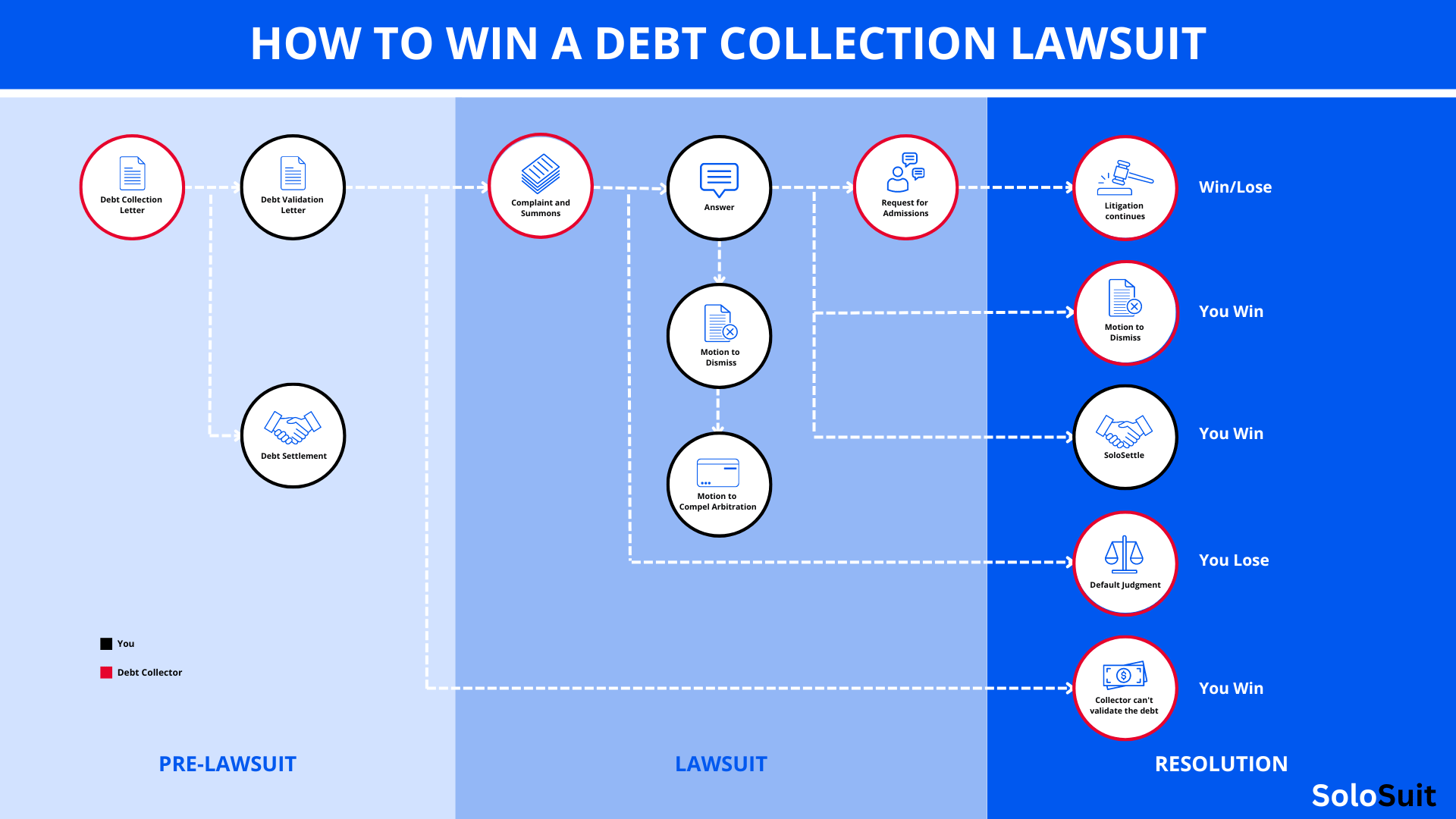

Debt Settlement with Lending Club

If you are carrying the heavy weight of debt and struggling to make ends meet, debt settlement may be a beacon of hope that can guide you toward financial freedom. Debt settlement is a process of negotiating with your creditors to pay less than the full amount you owe. While it may not be the ideal solution for everyone, it can be a lifeline for those who are facing overwhelming debt and have exhausted other options.

Lending Club, a prominent player in the financial realm, is a peer-to-peer lending platform that has facilitated connections between borrowers and investors. However, even the most diligent borrowers can encounter financial setbacks that make it challenging to keep up with their loan repayments. If you find yourself in this predicament with Lending Club, don’t lose hope. Debt settlement may be a viable path to resolving your debt and regaining financial stability.

Negotiating with Lending Club

To embark on the debt settlement journey with Lending Club, you will need to approach the company and express your inability to fulfill your repayment obligations. It’s crucial to be transparent about your financial situation and provide any relevant documentation that supports your request. Lending Club may consider factors such as your income, expenses, assets, and debt-to-income ratio when evaluating your eligibility for a settlement.

Negotiating a debt settlement with Lending Club is not a walk in the park. The company has its own policies and procedures for handling such requests. It’s advisable to seek guidance from a reputable credit counseling agency or a qualified attorney who specializes in debt settlement. They can assist you in crafting a compelling proposal and negotiating the best possible terms with Lending Club.

During the negotiation process, you may encounter resistance or even a flat-out rejection from Lending Club. However, don’t let that deter you. With patience, persistence, and a willingness to compromise, you can increase your chances of reaching a mutually acceptable agreement. Remember, the goal is to find a solution that alleviates your financial burden while also meeting the needs of Lending Club.

Tips for Negotiating a Debt Settlement

1. **Know your financial situation inside and out.** Before approaching Lending Club, gather all your financial documents and create a comprehensive budget that outlines your income, expenses, assets, and debts. This will empower you with a clear understanding of your financial standing and enable you to present a compelling case for debt settlement.

2. **Seek professional guidance.** Navigating the complexities of debt settlement alone can be daunting. Consider consulting a reputable credit counseling agency or an attorney who specializes in debt settlement. They can provide valuable guidance, protect your interests, and help you negotiate the best possible terms.

3. **Be prepared to compromise.** Debt settlement is not about getting off scot-free. Be prepared to negotiate a settlement amount that is less than the full amount you owe but still reasonable and affordable for you.

4. **Don’t give up.** The debt settlement process can be lengthy and challenging. However, don’t let setbacks discourage you. Stay persistent, and don’t give up on your goal of financial freedom.

Conclusion

Debt settlement with Lending Club can be a powerful tool for resolving overwhelming debt and regaining financial stability. By understanding the process, negotiating effectively, and seeking professional guidance when needed, you can increase your chances of a successful outcome. Remember, debt settlement is not a quick fix but a journey towards financial recovery. With determination and a commitment to rebuilding your finances, you can overcome the challenges and reach your destination.

Lending Club Debt Settlement: An Insight into Resolving Your Debt

If you’re struggling under the weight of high-interest debt, Lending Club debt settlement could be a lifeline you’ve been searching for. Debt settlement involves negotiating with your creditors to pay a lump sum that’s significantly less than the total amount you owe, offering a chance to break free from the shackles of overwhelming debt. However, before you jump into debt settlement, it’s imperative to understand its mechanics and potential implications.

Unveiling the Intricacies of Debt Settlement

Debt settlement is a process that enables you to settle your debts for a fraction of what you initially borrowed. It entails reaching an agreement with your creditors, typically through a debt settlement company, to pay a discounted sum in exchange for them discharging the remaining debt. This arrangement is legally binding, and once you’ve fulfilled the terms of the agreement, the debt is considered settled, and your credit report will reflect the settlement.

Exploring the Enigmatic World of Debt Settlement Companies

Debt settlement companies act as intermediaries between you and your creditors, negotiating on your behalf to secure a settlement. Their fees vary, but they typically charge a percentage of the amount saved through the settlement. While debt settlement companies can simplify the process, it’s crucial to choose a reputable one with a proven track record of success.

Laying Bare the Pros and Cons of Debt Settlement

Like any financial decision, debt settlement has its advantages and drawbacks. On the one hand, it offers a way to potentially reduce your debt burden and escape the cycle of high-interest payments. On the other hand, it can harm your credit score, and some creditors may be unwilling to negotiate. It’s essential to weigh the pros and cons carefully before deciding if debt settlement is the right path for you.

Navigating the Road to Debt Settlement

If you’re considering debt settlement, the first step is to contact a reputable debt settlement company. They will evaluate your financial situation and determine if you qualify for their services. If you do, they will negotiate with your creditors and help you develop a payment plan that fits your budget.

Once you’ve entered into a debt settlement agreement, it’s crucial to make your payments on time and in full. Failure to do so could jeopardize the agreement and damage your credit score even further. While debt settlement can be a viable option for managing overwhelming debt, it’s not a magic wand that will erase your financial woes overnight. It requires commitment, patience, and a willingness to face the potential consequences. By carefully considering all the factors and seeking professional guidance, you can make an informed decision about whether debt settlement is the right solution for you.

Lending Club Debt Settlement: A Path to Financial Freedom

Are you drowning in debt and struggling to find a way out? Lending Club debt settlement may be the solution you’ve been searching for. Debt settlement can help you reduce your debt burden, improve your credit score, and regain your peace of mind.

Benefits of Debt Settlement

There are several benefits to debt settlement, including:

* **Reduced debt burden:** Debt settlement can help you reduce your overall debt by up to 50%. This can free up your monthly cash flow and make it easier to manage your finances.

* **Improved credit score:** Debt settlement can also improve your credit score. When you settle your debts, your credit report will show that you have paid them off in full. This can help you qualify for lower interest rates on loans and credit cards in the future.

* **Peace of mind:** Debt settlement can give you peace of mind by eliminating the stress and anxiety of overwhelming debt. You’ll no longer have to worry about making minimum payments or facing collection calls.

How Does Debt Settlement Work?

Debt settlement is a process of negotiating with your creditors to reduce the amount of debt you owe. A debt settlement company can help you negotiate with your creditors and get them to agree to accept a lump sum payment that is less than the amount you owe.

If you’re considering debt settlement, it’s important to do your research and find a reputable company to work with. A good debt settlement company will have a proven track record of success and will be able to help you negotiate the best possible settlement for your situation.

Is Debt Settlement Right for You?

Debt settlement is not right for everyone. If you have a good credit score and you’re able to make your monthly payments on time, debt settlement may not be the best option for you. However, if you’re struggling to manage your debt and you’re looking for a way to get out of debt, debt settlement may be a good solution for you.

If you’re considering debt settlement, it’s important to talk to a credit counselor or a financial advisor to discuss your options. They can help you determine if debt settlement is right for you and help you create a plan to get out of debt.

Lending Club Debt Settlement

Lending Club is an online lending marketplace where borrowers can connect with investors to get personal loans. If you have a Lending Club loan that you’re struggling to repay, you may be considering debt settlement. Debt settlement is a process in which you negotiate with your creditors to pay less than the full amount you owe.

Risks of Debt Settlement

There are also some risks associated with debt settlement, including:

-

Damage to your credit score: Debt settlement can have a negative impact on your credit score, making it more difficult to get approved for loans, credit cards, and other forms of credit in the future.

-

Tax consequences: The amount of debt that you settle may be considered taxable income, meaning you could owe taxes on the forgiven debt.

-

Legal action from the creditor: If you can’t reach an agreement with your creditor, they may sue you for the full amount of the debt.

How to Avoid the Risks of Debt Settlement

There are a few things you can do to avoid the risks of debt settlement, including:

-

Get professional help: A credit counseling agency can help you negotiate with your creditors and develop a debt management plan that is right for you.

-

Make sure you understand the terms of the settlement: Before you agree to a debt settlement, make sure you understand the terms of the agreement and how it will affect your credit score and tax liability.

-

Don’t settle for less than you can afford: If you can’t afford to pay the full amount of your debt, don’t settle for less than you can afford. This could lead to more financial problems down the road.

Lending Club Debt Settlement: A Comprehensive Guide

Are you struggling with overwhelming Lending Club debt and exploring debt settlement as a possible solution? If so, this comprehensive guide will provide you with the essential steps and information you need to navigate this process effectively.

How to Settle Your Lending Club Debt

To initiate debt settlement with Lending Club, follow these steps:

1. **Reach out to Lending Club:** Call or write to Lending Club and clearly express your financial hardship.

2. **Document your situation:** Gather and provide documentation that supports your financial difficulties, such as proof of income, expenses, and medical bills.

3. **Negotiate a settlement amount:** Work with Lending Club to determine a reasonable settlement amount that you can afford.

What to Expect During the Settlement Process

Once you have initiated the debt settlement process with Lending Club, here’s what to expect:

1. **Review and accept the offer:** Lending Club will send you a settlement offer for your review. Carefully consider the terms and conditions before accepting.

2. **Make a lump-sum payment:** The settlement amount is typically paid in a single lump sum.

3. **Receive debt satisfaction:** Upon receiving your payment, Lending Club will mark your debt as satisfied and update your credit report accordingly.

Considerations Before Settling

Before deciding to settle your Lending Club debt, weigh the following considerations:

1. **Impact on credit score:** Debt settlement can negatively impact your credit score for up to seven years.

2. **Tax implications:** The settled debt may be considered taxable income and subject to taxes.

3. **Alternatives to settlement:** Explore other debt relief options, such as debt consolidation or credit counseling, before considering settlement.

Tips for Negotiating a Settlement

To negotiate a favorable settlement with Lending Club, keep these tips in mind:

1. **Be prepared:** Gather all necessary documentation and research industry benchmarks for settlement amounts.

2. **Communicate effectively:** Clearly explain your financial situation and emphasize your inability to repay the full amount.

3. **Be willing to compromise:** Settlement involves negotiation. Be prepared to concede on certain terms while holding firm on others.

Additional Resources

For further assistance with Lending Club debt settlement, consult the following resources:

1. **National Foundation for Credit Counseling:** https://www.nfcc.org/

2. **Consumer Financial Protection Bureau:** https://www.consumerfinance.gov/

Lending Club Debt Settlement: A Comprehensive Guide to Navigating Your Options

If you’re struggling with debt from Lending Club, you’re not alone. Many people find themselves in a similar situation, and there are various options available to help you manage your debt. One such option is debt settlement, which involves negotiating with your creditors to reduce the amount you owe. However, before you decide if debt settlement is right for you, it’s important to consider other alternatives that may be more suitable.

Insights into Lending Club Debt Settlement

Debt settlement can be a viable option if you’re unable to repay your debt in full. It involves working with a debt settlement company that negotiates with your creditors on your behalf. While it can help you reduce your debt, it’s crucial to be aware of the potential consequences. Debt settlement can negatively impact your credit score, and you may be required to pay taxes on the forgiven debt.

Exploring Alternatives to Debt Settlement

If you’re not sure whether debt settlement is right for you, there are other options available. Loan modification can help you adjust the terms of your loan, such as lowering your interest rate or extending your repayment period. Debt consolidation involves combining multiple debts into a single loan with a lower interest rate, making it easier to repay your debt over time. Bankruptcy is another option, but it’s important to seek legal advice before making this decision.

Loan Modification: Restructuring Your Debt

Loan modification is a good option if you’re facing short-term financial difficulties but want to keep your debt. It allows you to work with your lender to adjust the terms of your loan, making it more manageable. You may be able to lower your interest rate, extend your repayment period, or reduce your monthly payments. However, it’s important to note that loan modification is not always available, and it may not significantly reduce your overall debt.

Debt Consolidation: Combining Debts for Simplified Repayment

Debt consolidation involves taking out a new loan to pay off multiple existing debts. This can be a good option if you have high-interest debts or difficulty managing multiple payments. With debt consolidation, you’ll have a single monthly payment at a lower interest rate, making it easier to repay your debt. However, it’s important to compare different loan options and ensure that the new loan doesn’t come with high fees or penalties.

Bankruptcy: A Last Resort for Overwhelming Debt

Bankruptcy is a legal process that can provide you with relief from overwhelming debt. There are two main types of bankruptcy: Chapter 7 and Chapter 13. Chapter 7 involves liquidating your non-exempt assets to pay off your creditors. Chapter 13 allows you to create a repayment plan and make regular payments to your creditors. Bankruptcy can significantly impact your credit score and make it difficult to obtain credit in the future. However, it may be the right choice for individuals who are facing extreme financial hardship.

No responses yet