Introduction

When you’re buried in debt, it can feel like there’s no way out. You may be considering debt settlement or bankruptcy, but which one is right for you? Here’s a breakdown of the two options, so you can make an informed decision.

Debt settlement involves negotiating with your creditors to pay less than what you owe. Bankruptcy, on the other hand, is a legal proceeding that discharges your debts and gives you a fresh start. Which one is better for you depends on your specific circumstances.

Consequences of Debt Settlement vs. Bankruptcy

Debt settlement can damage your credit score, and it may take years to recover. Bankruptcy also has a negative impact on your credit score, but it’s typically not as severe as the damage caused by debt settlement. However, bankruptcy stays on your credit report for 10 years, while debt settlement stays on for seven.

Bankruptcy can also make it difficult to get a job, rent an apartment, or qualify for a loan. Debt settlement does not have these same consequences.

Which Option Is Right for You?

The best way to decide which option is right for you is to talk to a qualified professional. A bankruptcy attorney can help you understand the bankruptcy process and determine if it’s the right choice for you. A credit counselor can help you develop a debt management plan and explore other options for dealing with your debt.

Ultimately, the decision of whether to file for bankruptcy or settle your debts is a personal one. There is no right or wrong answer, and the best option for you will depend on your specific circumstances.

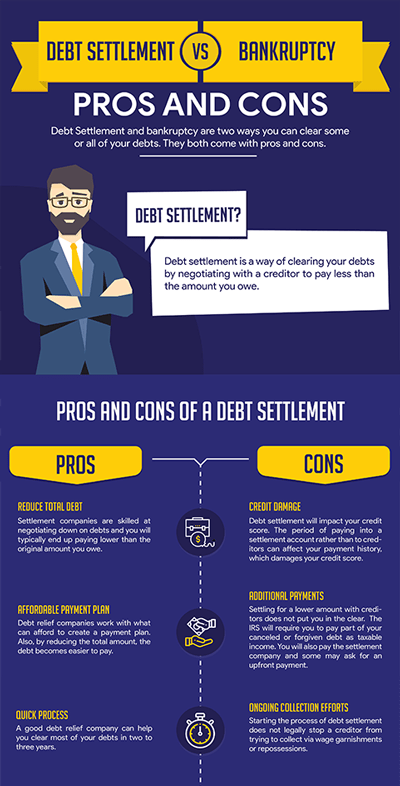

Pros and Cons of Debt Settlement

Pros:

Debt settlement can save you money. You may be able to negotiate a settlement for less than what you owe.

Debt settlement can help you get out of debt faster. You may be able to pay off your debts in a shorter period of time than you would if you filed for bankruptcy.

Cons:

Debt settlement can damage your credit score. It may take years to recover from the damage.

Debt settlement can be stressful. Negotiating with creditors can be a difficult and time-consuming process.

Pros and Cons of Bankruptcy

Pros:

Bankruptcy can discharge your debts. This means that you will no longer be legally obligated to pay them.

Bankruptcy can give you a fresh start. You can rebuild your credit and your life after bankruptcy.

Cons:

Bankruptcy can be expensive. You will need to pay attorney fees and court costs.

Bankruptcy can damage your credit score. It will stay on your credit report for 10 years.

What is the Better Option: Debt Settlement or Bankruptcy?

When faced with overwhelming debt, individuals may grapple with the dilemma of choosing between debt settlement and bankruptcy. Both options can provide relief, but they come with distinct advantages and drawbacks. Understanding the differences between them is crucial for making an informed decision.

Debt Settlement

Debt settlement involves negotiating with creditors to pay less than the full amount owed. The goal is to reach an agreement that significantly reduces the debt balance while avoiding the negative consequences associated with bankruptcy.

Debt settlement comes with several benefits. First, it allows individuals to avoid the stigma and long-term impact of bankruptcy on their credit scores. Second, it can provide a faster way to resolve debt than bankruptcy, which typically requires several years of court proceedings and payments. Third, debt settlement can potentially save individuals substantial sums of money compared to paying off the full debt amount.

However, debt settlement also has its drawbacks. One significant concern is the potential for creditors to refuse to negotiate or offer unfavorable settlement terms. Additionally, debt settlement can impact credit scores negatively in the short term, although they tend to recover faster than in bankruptcy. Finally, debt settlement fees can add up, reducing the amount of money individuals save.

Bankruptcy

Bankruptcy is a legal process that allows individuals to discharge or reorganize their debts. It can provide a complete or partial discharge of unsecured debts, such as credit card balances and medical bills. Filing for bankruptcy typically involves surrendering assets to a court-appointed trustee who distributes them among creditors.

Bankruptcy offers several advantages. First, it can provide a permanent discharge of certain debts. Second, it can stop creditors from pursuing collection efforts, such as wage garnishment or lawsuits. Third, bankruptcy can give individuals a fresh start and a chance to rebuild their financial lives.

Bankruptcy also has its drawbacks. One significant concern is the negative impact on credit scores, which can last for 10 years or more. Second, bankruptcy stays on an individual’s credit report for several years, making it difficult to obtain credit or loans in the future. Third, bankruptcy can be costly to file, and individuals may have to pay attorney fees, court costs, and other related expenses.

Conclusion

Ultimately, the decision between debt settlement and bankruptcy depends on an individual’s specific financial circumstances, goals, and risk tolerance. Debt settlement can be a viable option for those seeking to avoid bankruptcy and who have the ability to negotiate with creditors. Bankruptcy may be a more suitable choice for those with overwhelming debt or who face imminent legal action by creditors. Consulting with an experienced debt counselor or attorney can be invaluable in navigating the complexities of these options and making an informed decision.

**What’s Better: Debt Settlement or Bankruptcy?**

Are you struggling with overwhelming debt? If so, you may be considering debt settlement or bankruptcy as a way to get out from under it. Both options have their pros and cons, so it’s important to weigh them carefully before making a decision.

Bankruptcy

Bankruptcy is a legal proceeding that discharges all or part of your debts. There are two main types of bankruptcy: Chapter 7 and Chapter 13.

Chapter 7 bankruptcy liquidates your nonexempt assets to pay off your creditors. This means that you will lose all of your property, including your home, car, and savings. However, Chapter 7 bankruptcy can be a good option for people who have no assets and who are unable to repay their debts.

Chapter 13 bankruptcy allows you to repay your debts over a period of time. This type of bankruptcy is a good option for people who have some assets and who are able to make regular payments. However, Chapter 13 bankruptcy can be a long and expensive process.

Deciding whether to file for bankruptcy is a personal decision. There are many factors to consider, such as your financial situation, your goals, and your risk tolerance. If you are considering bankruptcy, it is important to talk to an attorney to get legal advice.

Debt Settlement

Debt settlement is a process of negotiating with your creditors to reduce the amount of debt that you owe. This can be a good option for people who have a lot of debt and who are unable to make regular payments. However, debt settlement can damage your credit score and make it difficult to obtain credit in the future.

When you enter into a debt settlement agreement, you will typically stop making payments to your creditors. Your creditors will then charge off the debt as a loss. This will damage your credit score, but it will also stop the collection process.

Debt settlement can be a good option for people who are unable to make regular payments and who are willing to accept the consequences of damaging their credit score. However, it is important to talk to a credit counselor or a debt settlement company before you make a decision.

Which is Better?

So, which is better: debt settlement or bankruptcy? The answer depends on your individual circumstances. If you have a lot of debt and are unable to make regular payments, debt settlement may be a good option. However, if you have a good credit score and are able to make regular payments, bankruptcy may be a better option. Ultimately, the best way to decide which option is right for you is to talk to an attorney or a credit counselor.

What’s Better: Debt Settlement or Bankruptcy?

When you’re drowning in debt, it can feel like you’re trapped in a never-ending cycle. You might be tempted to just give up and file for bankruptcy, but that’s not always the best solution. In some cases, debt settlement may be a better option. But how do you know which one is right for you?

Pros and Cons: Debt Settlement vs. Bankruptcy

Debt settlement is a process where you negotiate with your creditors to pay back less than the full amount you owe. This can be a good option if you can’t afford to make your full payments and you don’t want to file for bankruptcy. However, debt settlement can damage your credit score and it can take several years to complete.

Bankruptcy is a legal process that allows you to discharge your debts. This can be a good option if you have no other way to pay your debts. However, bankruptcy can also damage your credit score and it can make it difficult to get credit in the future.

Which Option Is Right for You?

The best option for you will depend on your individual circumstances. If you can afford to make your full payments, then you don’t need to consider either debt settlement or bankruptcy. However, if you can’t afford to make your full payments, then you should consider the following factors:

- Your credit score. Debt settlement can damage your credit score, while bankruptcy can damage it even more. If you have a good credit score, you may want to consider debt settlement instead of bankruptcy.

- Your income and expenses. If you have a low income and high expenses, then you may not be able to afford to make your full payments. In this case, bankruptcy may be a better option than debt settlement.

- Your assets. If you have assets, such as a home or a car, then you may want to consider debt settlement instead of bankruptcy. This is because bankruptcy can liquidate your assets.

Seeking Professional Help

If you’re not sure which option is right for you, then you should talk to a credit counselor or an attorney. They can help you evaluate your situation and make the best decision for your circumstances.

Which is Better: Debt Settlement or Bankruptcy?

If you are facing a mountain of debt, you may be wondering if debt settlement or bankruptcy is the better option for you. Both options have their pros and cons, so it’s important to weigh your choices carefully before making a decision.

Debt Settlement

Debt settlement is a process of negotiating with your creditors to pay back a portion of your debt. This can be a good option if you can’t afford to pay back your debts in full, but you want to avoid the negative consequences of bankruptcy.

** Pros of debt settlement:**

- You do not have to file for bankruptcy

- You pay less than your original debt

- It can help you get out of debt faster

Cons of debt settlement:

- It can hurt your credit score

- Your creditors may still sue you

- It can be difficult to find a reputable debt settlement company

Bankruptcy

Bankruptcy is a legal process that allows you to discharge your debts. This means that you will no longer be legally obligated to repay them. However, bankruptcy can have a negative impact on your credit score and make it difficult to get credit in the future.

Pros of bankruptcy:

- You can get rid of most of your debts

- It can stop creditors from harassing you

- It gives you a chance to rebuild your finances

Cons of bankruptcy:

- It can stay on your credit report for up to 10 years

- You may lose property or assets

- It can make it difficult to get credit or a job in the future

Which Option is Right for You?

The best way to decide which option is right for you is to speak to an attorney. An attorney can help you assess your situation and make the best decision for your circumstances.

Factors to Consider

When making your decision, you should consider the following factors:

- The amount of debt you have

- Your income and assets

- Your credit score

- Your future financial goals

- The advice of your attorney

Conclusion

If you are considering either debt settlement or bankruptcy, it is important to speak to an attorney to discuss your options and make the best decision for your situation.

No responses yet