Filing for bankruptcy is a major financial decision with significant consequences, and one of the most important factors to consider is how it will affect your credit. Here’s what you should know:

Immediate Impact:

- Filing for bankruptcy immediately triggers a "hard inquiry" on your credit report, which can lower your credit score by a few points.

- A bankruptcy notation will be added to your credit report, which can stay there for up to 10 years.

Short-Term Impact:

- Bankruptcy can lower your credit score significantly, making it difficult to qualify for loans, credit cards, and other forms of credit.

- Lenders may be hesitant to extend credit to you, even if you have a stable income and good repayment history.

Long-Term Impact:

- Over time, the negative impact of bankruptcy on your credit will gradually diminish.

- As positive payment history accumulates and the bankruptcy notation ages, your credit score will begin to improve.

- Bankruptcy can be a valuable tool for rebuilding your finances, but it’s important to understand how it will affect your credit in the short and long term.

Does Filing Bankruptcy Affect Your Credit?

If you’re struggling to make ends meet and considering filing for bankruptcy, one of the biggest concerns you likely have is how it will impact your credit. Understandably so, your credit score is a crucial factor in your financial well-being, and you don’t want to do anything that could damage it further. Fortunately, bankruptcy doesn’t have to be as detrimental to your credit as you might think. While it will temporarily lower your score, it can help you rebuild it over time.

Does Chapter 13 Bankruptcy Affect Your Credit?

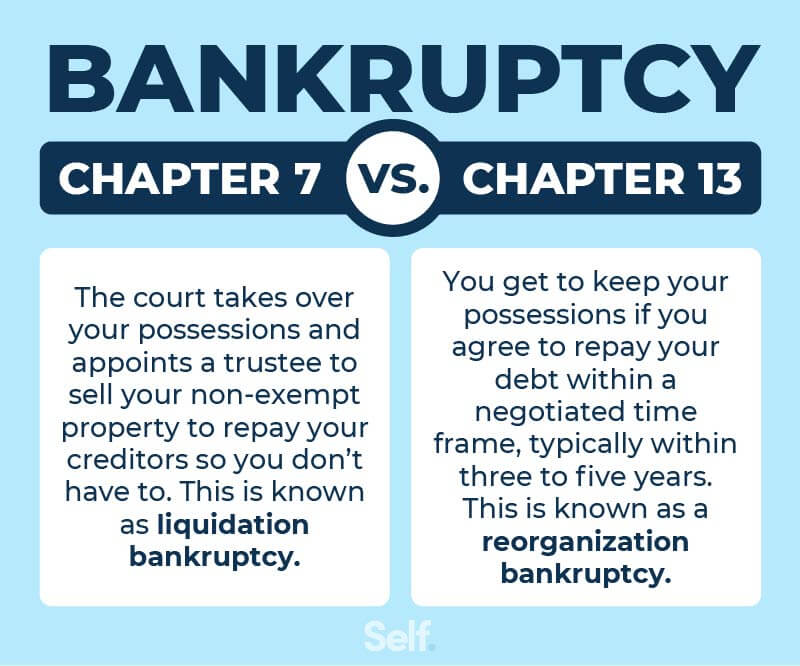

Chapter 13 bankruptcy is a reorganization bankruptcy that allows you to create a repayment plan to pay back your debts over a period of 3 to 5 years. Unlike Chapter 7 bankruptcy, which liquidates your assets to pay off your debts, Chapter 13 bankruptcy allows you to keep your property while you make your payments. This can be a good option for people who have a steady income and want to avoid losing their assets.

When you file for Chapter 13 bankruptcy, the automatic stay goes into effect. This means that your creditors cannot contact you or attempt to collect debts from you. You will also be assigned a Chapter 13 trustee who will oversee your repayment plan and make sure that you are making your payments on time. Your credit score will likely take a hit when you file for Chapter 13 bankruptcy, but it will start to improve as you make your payments on time. Once you have completed your repayment plan, your credit score should be back to where it was before you filed for bankruptcy.

Does Filing Bankruptcy Affect Your Credit?

The answer is a resounding yes. Filing for bankruptcy will have a significant impact on your credit score and can make it difficult to obtain credit in the future.

Does Chapter 7 Bankruptcy Affect Your Credit?

Chapter 7 bankruptcy is the most common type of bankruptcy filed by individuals. It involves liquidating your assets (with exemptions) to pay back your debts. As you might imagine, having a Chapter 7 bankruptcy on your record is like a big red flag to lenders. It’s a clear indication that you have had significant financial problems. As a result, your credit score can take a nosedive, typically dropping by 100 to 200 points. The negative impact can last for up to 10 years, making it difficult to obtain credit or qualify for favorable interest rates during that period.

Does Filing Bankruptcy Affect Your Credit?

Can you keep a secret for a decade? Filing for bankruptcy certainly will for that long, at least on your credit report. Bankruptcy is a serious financial move that can have far-reaching consequences, including a significant hit to your credit score. But just how long does this black mark stay on your record? Here’s the lowdown on how bankruptcy affects your credit and how long it sticks around.

How Long Does Bankruptcy Stay on Your Credit Report?

Once you file for bankruptcy, the clock starts ticking. Bankruptcy stays on your credit report for a whopping 10 years from the date of filing. That’s a long time to have such a blemish on your record, but it’s important to remember that it will eventually fall off. That’s why, if you file for bankruptcy, you should focus on rebuilding your credit as soon as possible so you can minimize the long-term damage to your credit score.

How to Rebuild Your Credit After Bankruptcy

Rebuilding your credit after bankruptcy takes time and effort, but it’s definitely possible. Here are a few tips to get you started:

- Start with a secured credit card. This type of card is backed by a cash deposit, which reduces the risk to the lender. Once you’ve made a few on-time payments, you may be able to upgrade to an unsecured card.

- Become an authorized user on someone else’s credit card. This is a great way to build your credit without having to open a new account in your own name.

- Take out a small loan. A small personal loan or credit-builder loan can help you establish a positive payment history.

Rebuilding your credit after bankruptcy won’t happen overnight, but with patience and persistence, you can improve your credit score and get back on the road to financial recovery.

Does Filing Bankruptcy Affect Your Credit? Here’s What You Need to Know

In the financial world, few things have the same impact as filing for bankruptcy. It’s a drastic measure that can have a profound effect on your credit, your finances, and your future. The weight of such a decision can be daunting, and it’s essential to understand the full extent of the consequences before taking that step. Particularly, it’s crucial to know how bankruptcy can impact your credit – the lifeblood of your financial standing.

Filing for bankruptcy is like hitting the reset button on your credit, but it comes with a hefty price. Your credit score takes a significant nosedive, making it harder to access credit, secure loans, or even rent an apartment. Bad credit can linger for up to 10 years, casting a long shadow over your financial future.

So, if bankruptcy is on your mind, proceed with caution. Weigh the pros and cons carefully, and seek professional advice from a credit counselor or attorney. Bankruptcy should be a last resort, and it’s critical to explore all other options before making that decision.

Can You Get a Mortgage After Bankruptcy?

Getting a mortgage after bankruptcy is an uphill battle, but it’s not impossible. Lenders will scrutinize your credit history with a microscope, and you’ll likely face higher interest rates and stricter terms. The waiting period after bankruptcy can vary, but it typically takes at least two years before you’re eligible for a mortgage. Even then, it’s essential to have a strong post-bankruptcy credit history and a steady income to qualify.

If you’re determined to buy a home after bankruptcy, start by rebuilding your credit. Pay your bills on time, every time. Keep your credit utilization low, and avoid taking on new debt. It will take time and effort, but it’s the only way to improve your chances of getting approved for a mortgage.

Does Filing Bankruptcy Affect Your Credit?

Filing bankruptcy can be a difficult and stressful decision, but it’s important to understand how it might impact your credit. Bankruptcy is a legal proceeding that allows individuals to discharge debts they can’t repay. However, it also has severe consequences for your credit score.

How Bankruptcy Affects Your Credit

Bankruptcy remains on your credit report for seven to ten years, depending on the type of bankruptcy filed. This can make it difficult to obtain credit in the future, as lenders view bankruptcy as a red flag indicating financial instability. Your credit score will likely drop significantly after filing for bankruptcy, making it harder to qualify for loans and credit cards with favorable terms.

Rebuilding Your Credit After Bankruptcy

Rebuilding your credit after bankruptcy takes time and effort. The first step is to create a budget and stick to it, paying bills on time and reducing debt. Consider getting a credit builder loan, which is a small loan designed to help you rebuild your credit history. Gradually, you can start to reestablish your credit by making regular payments and using credit responsibly.

Five Key Factors That Impact Your Credit After Bankruptcy

-

Type of Bankruptcy: Filing for Chapter 13 bankruptcy, which involves repaying debts over time, has less of an impact on your credit than Chapter 7, which liquidates assets to pay off debts.

-

Previous Credit History: A history of good credit before bankruptcy can help mitigate the negative impact on your score.

-

Length of Time Since Bankruptcy: The longer it’s been since you filed for bankruptcy, the less it will affect your credit score.

-

New Credit History: Building a positive credit history after bankruptcy is crucial. Make on-time payments and keep balances low.

-

Financial Situation: Lenders will consider your overall financial situation, including your income, expenses, and assets, when assessing your creditworthiness after bankruptcy.

Conclusion

Filing bankruptcy is a last resort for those struggling with overwhelming debt. While it can provide temporary relief, it also has long-term consequences for your credit. Understanding the impact of bankruptcy on your credit can help you make an informed decision and begin rebuilding your financial foundation after this challenging experience.

No responses yet