Debt Consolidation Loan vs. Debt Settlement: Understanding the Options

Are you struggling under the weight of unmanageable debt? If so, you may be considering debt consolidation or debt settlement as a way to get out of the financial hole you’re in. Both options have their own unique advantages and disadvantages, so it’s important to understand the differences before making a decision. Sit down, buckle up, and let’s dive into the exciting world of debt elimination!

Debt Consolidation Loan

A debt consolidation loan is a personal loan that you can use to pay off your existing debts. This can be a good option if you have multiple debts with high interest rates. By consolidating your debts into and merging’em into one loan with a lower interest rate, you can potentially save money on interest and pay off your debt faster. However, you’ll need to qualify for a debt consolidation loan, and the interest rate you’re offered will depend on your credit score. Consolidation loans can sometimes act like a band-aid on a bullet wound, so it’s important to address the underlying issues that led to the debt in the first place. Otherwise, you may find yourself back in the same boat down the road.

Debt Settlement

Debt settlement is an agreement with your creditors to pay a lump sum that is less than the amount you actually owe. This can be a good option if you’re unable to repay your debts in full. However, debt settlement can damage your credit score and make it difficult to get credit in the future. It’s also important to note that debt settlement companies often charge high fees, so it’s important to do your research before signing up with one. Debt settlement is like taking a shortcut through a dark forest. It might seem tempting, but it can be fraught with peril. You may emerge on the other side owing less money, but your credit score, that beacon of financial well-being, could be left in tatters.

Which is Better: Debt Consolidation Loan vs. Debt Settlement?

Are you struggling to keep your head above water with multiple debts? You’re not alone. Millions of Americans are facing the same dilemma. If you’re considering debt consolidation or debt settlement, it’s important to understand the pros and cons of each option so you can make an informed decision. Some common methods used to manage debt are debt consolidation loans and debt settlements. These options both have their pros and cons but which one is best for you? The answer depends on your unique financial situation.

Types of Debt Management Options

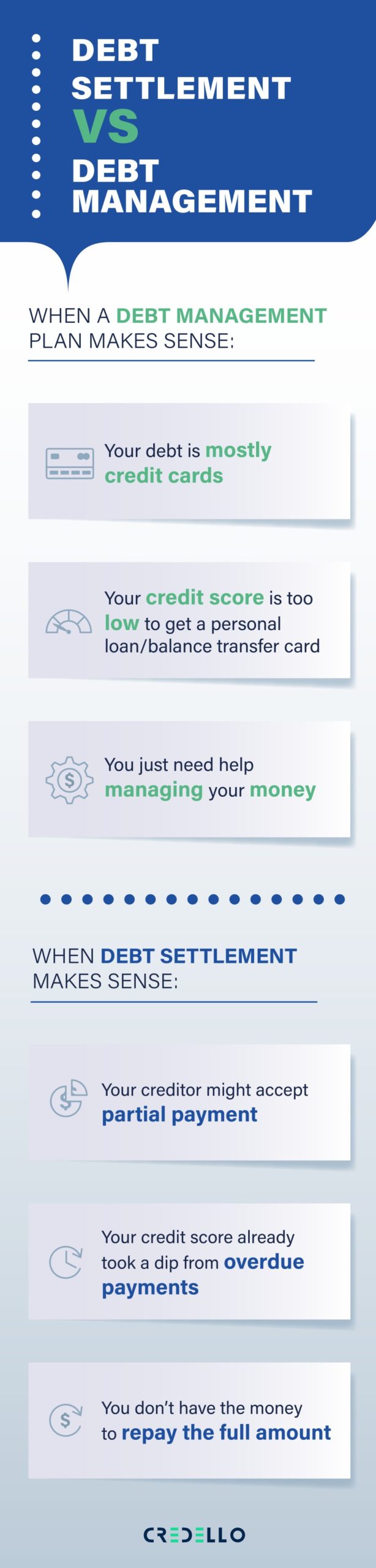

There are a number of different debt management options available, including debt consolidation loans, debt settlement, and debt management plans. Debt consolidation loans allow you to combine multiple debts into a single loan with a lower interest rate. Debt settlement involves negotiating with your creditors to pay off your debts for less than the full amount you owe. Debt management plans allow you to make regular payments to a credit counseling agency, which then distributes the funds to your creditors.

Debt Consolidation Loans

Debt consolidation loans are a good option for people who have multiple debts with high interest rates. Debt consolidation loans can help you save money on interest and make it easier to manage your debt payments. However, debt consolidation loans can also have some drawbacks. For example, you may have to pay a higher interest rate than you would on a traditional loan. Additionally, if you have bad credit, you may not qualify for a debt consolidation loan.

Debt Settlement

Debt settlement is a good option for people who are struggling to make their debt payments. For instance, folks who are on the brink of bankruptcy may want to consider debt settlement. Debt settlement can help you get out of debt for less than the full amount you owe. However, debt settlement can also damage your credit score. Additionally, you may have to pay taxes on the amount of debt that is forgiven.

Which Option Is Right for You?

The best debt management option for you will depend on your specific financial situation. If you have multiple debts with high interest rates, a debt consolidation loan may be a good option. If you are struggling to make your debt payments, debt settlement may be a good option. To determine the best option, you need to consider variables such as your budget, timeline, income, credit score, and other financial obligations.

Debt Consolidation Loan vs. Debt Settlement

Ugh, debt — it can feel like a never-ending cycle. If you’re drowning in debt, you might consider options like debt consolidation loans or debt settlement. But which is right for you? Let’s dive into the details to help you make an informed decision.

Debt Consolidation Loans

A debt consolidation loan is like a financial superhero that combines your multiple debts into a single loan. Imagine having a bunch of unruly debts scattered across numerous accounts, each with different interest rates and due dates. Debt consolidation loans swoop in and consolidate these debts into one easy-to-manage loan, typically with a lower interest rate. It’s like organizing a messy closet — everything in its place, and peace of mind restored!

However, debt consolidation loans aren’t magic wands. You still need to make regular payments, and there can be fees associated with the loan, such as origination fees or closing costs. It’s important to carefully review the loan terms before signing on the dotted line.

Debt Consolidation Loan vs. Debt Settlement: Demystifying Your Options

Like a hiker struggling up a steep slope, finding a way out of debt can be arduous. But don’t despair, there are two viable paths that can lead you to financial freedom: debt consolidation loans and debt settlement.

Debt Consolidation Loan: Regrouping Your Debts

Picture this: multiple credit card balances, each with a different interest rate and payment due date. It’s a recipe for financial chaos. Enter the debt consolidation loan – a lifeline that allows you to roll all those unruly debts into one convenient monthly payment with a potentially lower interest rate. It’s like bringing harmony to a financial symphony!

Debt Settlement: Striking a Deal

If your debt burden feels unsurmountable, debt settlement may offer a glimmer of hope. By enlisting the help of a debt settlement company, you can negotiate with creditors to reduce your outstanding balances. It’s like a financial game of chicken, where you dance on the edge of default to secure a more manageable sum. But be warned, debt settlement can damage your credit report and make it tougher to borrow in the future.

Choosing the Right Path: A Crossroads of Finance

To determine which option is right for you, ask yourself: “How long can I afford to wait?” If your financial situation is dire and you need immediate relief, debt settlement may be your best bet, despite the potential credit hit. On the other hand, if you have the patience and a steady income, a debt consolidation loan can provide a more structured and less damaging route to debt freedom.

Beware of Pitfalls: The Perils of Quick Fixes

Remember, debt settlement is not a magical wand that can erase your debts overnight. It’s a process that requires patience, perseverance, and a keen understanding of the potential consequences. Don’t fall prey to unscrupulous debt settlement companies that promise instant results and charge exorbitant fees. The path to debt freedom should be paved with caution and informed decisions.

Conclusion: Seeking Professional Guidance

Navigating the treacherous waters of debt can be overwhelming. Don’t hesitate to seek professional guidance from a certified credit counselor or a reputable debt settlement company. They can provide impartial advice and help you determine the best course of action for your unique financial situation. Remember, you’re not alone on this journey towards financial liberation. With the right tools and determination, you can conquer your debts and reclaim your financial well-being.

**Debt Consolidation Loan vs. Debt Settlement: Which Is Right for You?**

Trying to figure out how to get out of debt? You’re not alone. Millions of Americans are struggling with crushing debt. If you’re one of them, you may be considering debt consolidation or debt settlement. But which one is right for you?

**Debt Consolidation Loan**

With a debt consolidation loan, you take out a new loan to pay off your existing debts. This can simplify your monthly payments and potentially lower your interest rate. However, you’ll still be responsible for repaying the full amount of your debt, plus interest.

**Debt Settlement**

With debt settlement, you negotiate with your creditors to pay less than what you owe. This can be a good option if you’re struggling to make your payments and can’t afford to pay off your debt in full. However, debt settlement can damage your credit score and make it difficult to get credit in the future.

**Factors to Consider**

When choosing between debt consolidation and debt settlement, consider the following factors:

**1. Your Financial Situation**

Are you able to make regular payments on a debt consolidation loan? If not, debt settlement may be a better option.

**2. The Amount of Debt**

If you have a large amount of debt, debt consolidation may not be a viable option. Debt settlement may be a better choice if you owe more than you can afford to repay.

**3. The Terms of the Available Options**

Carefully compare the terms of the debt consolidation loan and debt settlement options that are available to you. Consider the interest rates, fees, and repayment terms.

**4. Potential Impact on Your Credit Score**

Debt settlement can damage your credit score. If you’re concerned about your credit score, debt consolidation may be a better option.

**5. Your Long-Term Goals**

Do you plan to buy a home or car in the near future? If so, debt consolidation may be a better option because it can help you improve your credit score.

**Which Is Right for You?**

The best way to decide which option is right for you is to talk to a financial advisor. They can help you assess your financial situation and make the best decision for your needs.

Debt Consolidation Loan vs. Debt Settlement: Which Is Right for You?

If you’re drowning in debt, you may be considering debt consolidation or debt settlement to get your finances back on track. But which one is right for you? Here’s a breakdown of the advantages and disadvantages of each option to help you make an informed decision.

Debt Consolidation Loans

Debt consolidation loans are personal loans that you can use to pay off your existing debts. This can simplify your monthly payments and potentially save you money on interest. Additionally, making timely payments on a debt consolidation loan can help you rebuild your credit.

Debt Settlement

Debt settlement is an agreement with your creditors to pay back less than the full amount you owe. This can significantly reduce your debt, but it can also damage your credit score. Additionally, debt settlement companies may charge high fees, so it’s important to weigh the pros and cons carefully.

Advantages and Disadvantages

| Feature | Debt Consolidation Loan | Debt Settlement |

|---|---|---|

| Interest rates | Lower | Varies |

| Impact on credit score | Can improve | Can damage |

| Fees | Typically low | Can be high |

| Amount of debt reduced | Varies | Can significantly reduce debt |

| Timeframe | Can take several years | Can be completed in a few months |

| Eligibility | Must have good credit | Available to those with poor credit |

Which Option Is Right for You?

The best option for you depends on your individual circumstances. If you have good credit and can qualify for a low-interest debt consolidation loan, it may be the better option. However, if you have poor credit or a lot of debt, debt settlement may be a better choice.

Tips for Choosing a Debt Consolidation or Debt Settlement Company

If you decide to pursue debt consolidation or debt settlement, it’s important to choose a reputable company. Here are a few tips:

- Do your research. Read reviews and compare different companies before making a decision.

- Get a free consultation. This will give you a chance to learn more about the company and its services.

- Be wary of high fees. Some companies charge excessive fees, so be sure to get a clear understanding of the costs involved before signing up.

- Get everything in writing. Make sure you understand the terms of your agreement before signing anything.

Debt Consolidation Loans vs. Debt Settlement: Unraveling the Maze

In today’s financial landscape, managing debt can be a daunting task. When faced with overwhelming obligations, individuals often grapple with the dilemma of choosing between debt consolidation loans and debt settlement. Each option presents its own set of advantages and drawbacks, and the ideal choice hinges on personal circumstances and financial objectives.

Debt Consolidation Loans: Managing Debt Without the Drama

A debt consolidation loan acts as a soothing balm for scattered debts. It’s like merging all your obligations into one, manageable payment. This streamlined approach simplifies budgeting and can lead to lower interest rates, potentially saving you money. Plus, it boosts your credit score by reducing the number of accounts with outstanding balances.

Debt Settlement: A Drastic Solution for Dire Straits

Debt settlement, on the other hand, is a bit more like playing hardball with your creditors. It entails negotiating a reduced payoff amount, typically for less than what you owe. While it can provide quick relief from debt, it comes with a hefty price tag: a substantial hit to your credit score.

Picking Your Path: A Maze of Considerations

Choosing between these options is like navigating a financial maze. Here are some crucial factors to keep in mind:

1. Debt-to-Income Ratio

This metric measures how much of your income is dedicated to debt payments. A high ratio may make debt consolidation more challenging to qualify for.

2. Credit Score

A solid credit score is usually a prerequisite for debt consolidation loans with favorable terms. If your score is less than stellar, debt settlement may be your only option.

3. Long-Term Financial Goals

Debt settlement can damage your credit, potentially impacting future borrowing. If maintaining a good credit score is paramount, debt consolidation may be the wiser choice.

4. Debt Amount

Debt consolidation loans typically have lower limits than debt settlement. If your debt exceeds the loan limit, settlement could be your solution.

5. Time Horizon

Debt consolidation is a long-term solution, while debt settlement can provide faster relief. Consider your time frame when making your decision.

6. Emotional Toll

Debt settlement involves intense negotiations and potential legal implications. Be prepared for an emotional rollercoaster if you choose this route.

7. Impact on Credit Score

Debt settlement can significantly lower your credit score. If your credit is crucial for future financial endeavors, think twice before pursuing this option. Debt consolidation, on the other hand, can ultimately boost your credit score.

No responses yet