**Credit Counseling vs. Debt Settlement: Finding the Right Path Out of Debt**

Credit counseling and debt settlement are two options available to individuals struggling with debt. While both strive to help people regain financial stability, they differ in approach and outcomes. Determining the best choice depends on one’s circumstances and needs.

Credit Counseling

Credit counseling is a comprehensive service offered by non-profit agencies. It’s designed to provide personalized guidance and support to individuals facing debt challenges. During counseling sessions, individuals work with certified counselors to assess their financial situation, develop a realistic budget, and create a plan for managing debt.

Counselors can assist with identifying income and expenses, negotiating with creditors, and exploring repayment options. They also provide education on financial management, budgeting, and the responsible use of credit. The goal of credit counseling is to empower individuals with the knowledge and tools necessary to regain control over their finances and become debt-free.

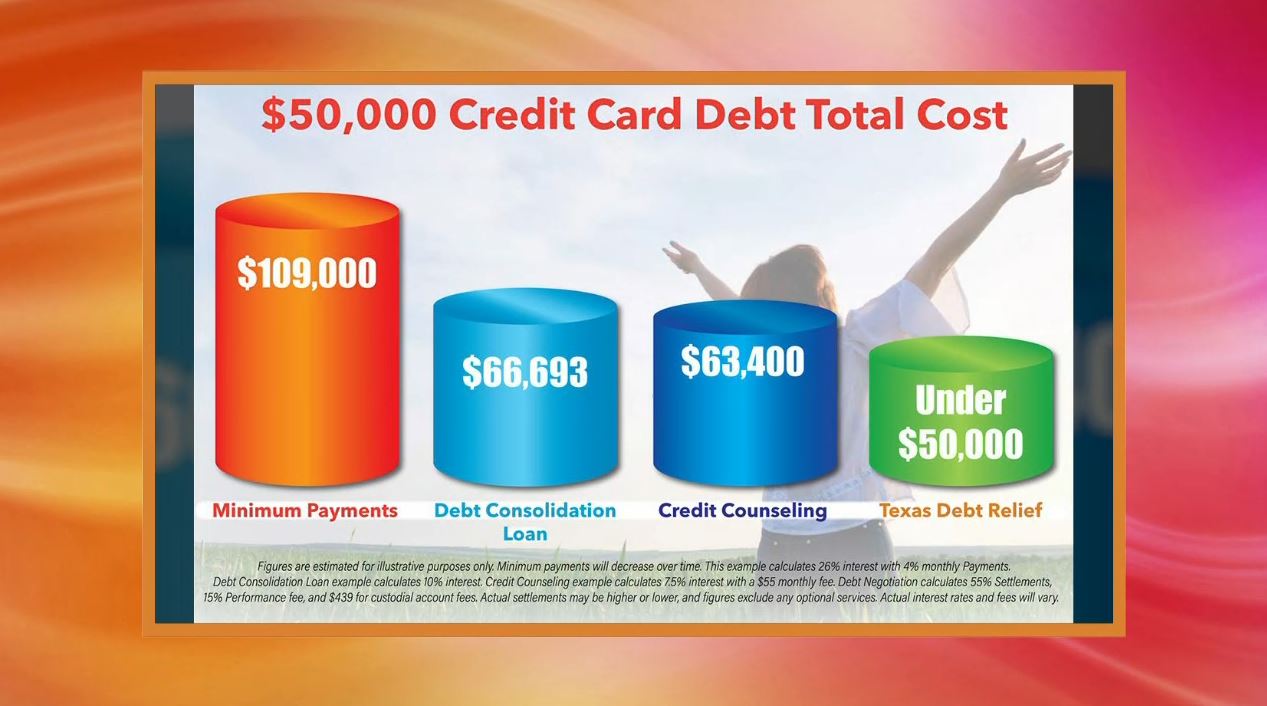

Benefits of credit counseling include:

– **Personalized guidance:** Counselors provide tailored advice berdasarkan on individual circumstances.

– **Negotiation assistance:** Counselors can help mediate between individuals and creditors to reduce interest rates, fees, and payment amounts.

– **Financial education:** Counseling sessions cover budgeting, debt management, and credit repair strategies.

– **Long-term support:** Agencies often provide ongoing support and resources to individuals as they navigate their journey towards becoming debt-free.

Credit Counseling vs. Debt Settlement

Whether you’re struggling to make ends meet or facing overwhelming debt, there are several options to help you get back on track. Two popular choices are credit counseling and debt settlement. But what’s the difference between the two, and which one is right for you? Let’s take a closer look.

Debt Settlement

Debt settlement is a process where you negotiate with your creditors to pay less than the full amount you owe. This can be a good option if you’re struggling to make your monthly payments and don’t have the means to pay off your debt in full. However, it’s important to note that debt settlement can have a negative impact on your credit score, and you may have to pay taxes on the amount of debt that is forgiven.

There are a few different ways to negotiate a debt settlement. One option is to work with a debt settlement company. These companies will negotiate with your creditors on your behalf and may be able to get you a lower settlement amount. However, you will need to pay a fee to the debt settlement company, which can range from 15% to 25% of the amount of debt that is settled.

Another option is to negotiate directly with your creditors. This can be a more difficult process, but it can save you money on fees. If you decide to negotiate directly with your creditors, be sure to get everything in writing before you make any payments.

It’s important to weigh the pros and cons of debt settlement carefully before you decide if it’s the right option for you. Debt settlement can be a good way to reduce your debt and get your finances back on track, but it’s important to do your research and understand the potential risks and benefits before you make a decision.

No responses yet