When you’re facing overwhelming debt, it can be difficult to know which option is best for you. Two common choices are debt management and debt settlement. Both options have their own pros and cons, so it’s important to understand the differences before making a decision.

**Debt Management**

Debt management is a process of working with a credit counseling agency to create a repayment plan that fits your budget. The agency will negotiate with your creditors to lower your interest rates and monthly payments. Debt management can help you get out of debt faster and save money on interest charges. However, it can also affect your credit score and may take several years to complete.

**Debt Settlement**

Debt settlement is a process of negotiating with your creditors to pay less than the full amount you owe. This can be a good option if you’re unable to make your monthly payments and are facing foreclosure or bankruptcy. However, debt settlement can damage your credit score and may take several years to complete.

**Which Option Is Best for You?**

The best option for you depends on your individual circumstances. If you’re able to make your monthly payments and want to improve your credit score, debt management may be a good option. If you’re unable to make your monthly payments and are facing foreclosure or bankruptcy, debt settlement may be a good option.

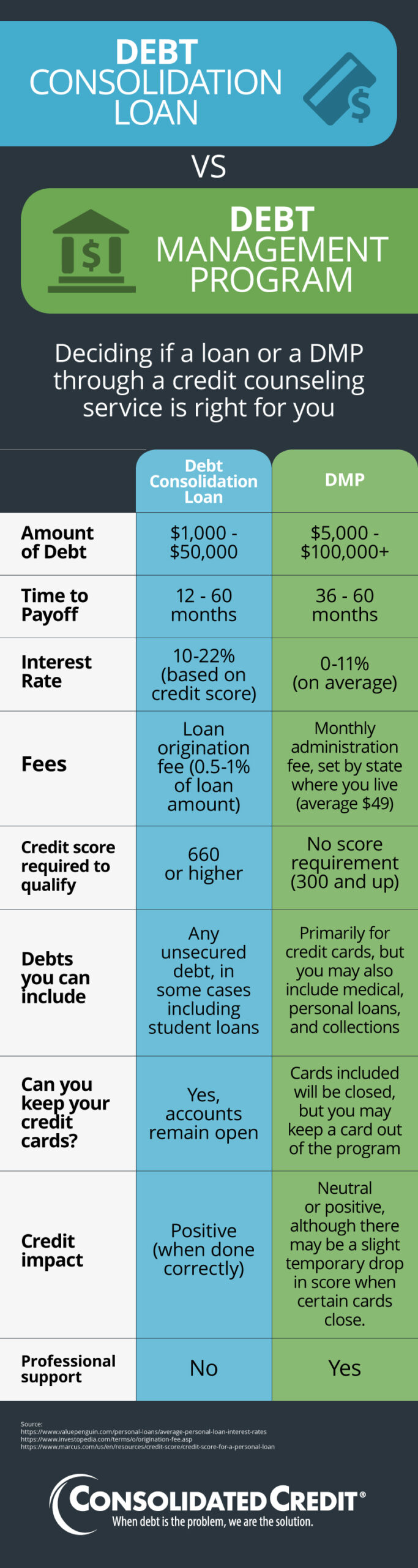

**Here’s a table that summarizes the key differences between debt management and debt settlement:**

| Feature | Debt Management | Debt Settlement |

|—|—|—|

| How it works | Negotiate lower interest rates and monthly payments | Negotiate to pay less than the full amount owed |

| Effect on credit score | Can negatively affect your credit score | Can damage your credit score |

| Time to complete | Can take several years to complete | Can take several years to complete |

**No matter which option you choose, it’s important to work with a reputable credit counseling agency or debt settlement company. These companies can help you understand your options and make the best decision for your financial situation.**

Debt Management vs. Debt Settlement: Which is Right for You?

Are you drowning in a sea of debt and wondering which lifeline to grab? Debt management and debt settlement are two common options, but they’re like two sides of a coin—completely different in their approach and consequences. It’s like comparing apples to oranges—each one has its own unique flavor.

Pros and Cons of Debt Management

Debt management, essentially a financial rehab, is a structured program that helps you manage your debt by consolidating it into one monthly payment. This simplifies your bills and can lower your interest rates, giving you some breathing room. But like any loan, debt management comes with a repayment period. Plus, you’ll have to pay fees for the program, which can add up over time and potentially offset any savings you make on interest. And here’s the kicker: if you don’t stick to the plan, your debt could spiral out of control again.

Pros and Cons of Debt Settlement

Debt settlement is more drastic than debt management. It involves negotiating with your creditors to pay back less than you actually owe. This can be a lifesaver for those buried under a mountain of debt they can’t afford to repay, as it can significantly reduce their overall debt burden. But here’s the catch: debt settlement can severely damage your credit score, making it harder to borrow money in the future. Additionally, the IRS may consider the forgiven debt as taxable income, potentially adding more stress to your financial situation.

So, Which One is Right for You?

The best debt relief option depends on your specific circumstances. Debt management is a more conservative approach that preserves your credit but requires regular payments over an extended period. Debt settlement is a more aggressive solution that can significantly reduce your debt but comes with a hefty hit to your credit score. Ultimately, the choice is yours but do your homework before taking the plunge. Weigh the pros and cons carefully to ensure you make the decision that’s right for you.

Which is Better: Debt Management or Debt Settlement?

Are you drowning in debt? Finding yourself struggling to keep up with multiple monthly payments? If you’re like millions of Americans, you may be considering debt management or debt settlement as a way to get back on track financially. But which option is right for you? Here’s a breakdown of each to help you make an informed decision:

Debt Management

Debt management is a process of consolidating your debts into a single monthly payment, typically at a lower interest rate. This can make it easier to budget and pay off your debt faster. There are two main types of debt management:

- Credit counseling: A non-profit credit counseling agency can work with you to create a debt management plan. They will negotiate with your creditors on your behalf to lower your interest rates and monthly payments.

- Debt consolidation loan: A debt consolidation loan is a personal loan that you can use to pay off your other debts. This can simplify your monthly payments and potentially save you money on interest.

There are several benefits to debt management. It can help you:

- Lower your interest rates

- Reduce your monthly payments

- Consolidate your debts into a single payment

- Improve your credit score (if you make your payments on time)

However, there are also some potential drawbacks to debt management. It can take several years to pay off your debts through debt management, and you may have to pay additional fees to the credit counseling agency or lender.

Which is Better: Debt Management or Debt Settlement?

When you find yourself overwhelmed by debt, it can feel like you’re drowning in a sea of bills. You may be wondering if there’s any way out, and if so, what’s the best way to do it.

Two common debt relief options are debt management and debt settlement.

So, which one is right for you? In this article, we’ll compare the pros and cons of each option to help you make an informed decision.

Debt Settlement

Debt settlement is a process of negotiating with your creditors to pay less than the amount you owe. This can be a good option if you’re facing a large amount of debt and you’re unable to make the minimum payments. However, it’s important to know that debt settlement can have a negative impact on your credit score.

The Pros of Debt Settlement

There are a few potential benefits to debt settlement, including:

The Cons of Debt Settlement

There are also some potential drawbacks to debt settlement, including:

Debt Management

Debt management is a process of working with a credit counseling agency to create a plan to pay off your debt. This can be a good option if you’re struggling to make your minimum payments, but you don’t want to damage your credit score.

The Pros of Debt Management

There are a few potential benefits to debt management, including:

The Cons of Debt Management

There are also some potential drawbacks to debt management, including:

No responses yet