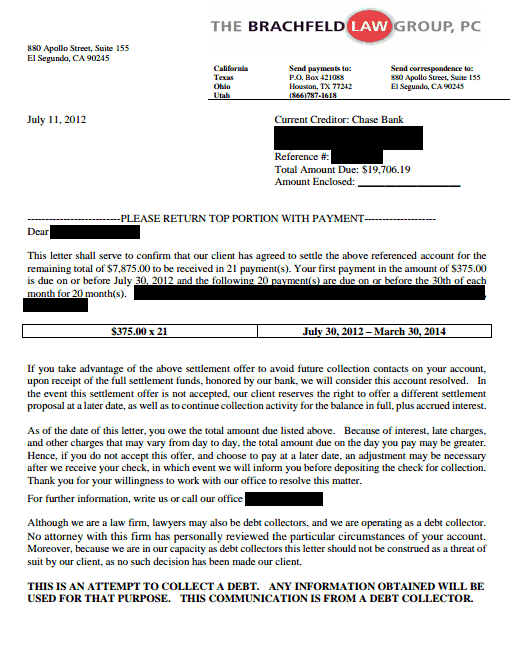

Chase Debt Settlement: Digging into Your Options

Are you buried under a mountain of Chase credit card debt, wondering if there’s a way to escape without paying back every last penny? Well, buckle up, folks, because debt settlement might just be your financial lifeline.

What is Chase Debt Settlement?

Picture this: you and Chase, sitting down at a negotiation table, hammering out a deal where you pay a fraction of your outstanding balance to settle your debt. That, in a nutshell, is debt settlement. It’s not a magic wand that makes your debt disappear, but it can significantly reduce the amount you owe and give you a fresh financial start.

Now, let’s dive into the nitty-gritty. Chase debt settlement involves negotiating with Chase directly or through a debt settlement company. You’ll propose a lump-sum payment that’s less than your total debt, and if Chase accepts, you’ll be off the hook for the remaining balance.

But here’s the catch: debt settlement can impact your credit score and may not be the best option for everyone. Before you jump in, it’s crucial to weigh the pros and cons carefully and consider other debt management strategies.

Is Chase Debt Settlement Right for You?

Are you struggling to make ends meet and keep up with your Chase credit card payments? If so, you may be wondering if debt settlement is the right option for you. Debt settlement is a process of negotiating with your creditors to reduce the amount of money you owe. It can be a good option if you’re facing serious financial hardship and are unable to repay your debts in full.

There are a few things to keep in mind before you decide if debt settlement is right for you. First, it’s important to understand that debt settlement can have a negative impact on your credit score. Your score may drop significantly, which can make it difficult to qualify for future loans or credit cards. Second, you may have to pay taxes on the amount of debt that is forgiven. Finally, debt settlement can take several months or even years to complete.

Pros and Cons of Chase Debt Settlement

There are both pros and cons to Chase debt settlement. Some of the pros include:

- You may be able to reduce the amount of money you owe by up to 50% or more.

- You can stop making payments on your debts while you’re negotiating a settlement.

- Debt settlement can help you get out of debt faster than if you continued to make minimum payments.

Some of the cons of Chase debt settlement include:

- Your credit score will likely drop significantly.

- You may have to pay taxes on the amount of debt that is forgiven.

- Debt settlement can take several months or even years to complete.

How to Negotiate a Chase Debt Settlement

If you’re considering Chase debt settlement, there are a few things you can do to increase your chances of success. First, you’ll need to gather all of your financial information, including your income, expenses, and debts. You’ll also need to provide Chase with a hardship letter explaining why you’re unable to repay your debts. Once you have all of your information together, you can contact Chase and begin the negotiation process. Keep in mind, the more organized and prepared you are, the easier the process will be.

Negotiating a Chase debt settlement can be a long and challenging process. However, if you’re facing serious financial hardship, it may be the best option for you. By following these tips, you can increase your chances of success.

Chase Debt Settlement: Weighing the Pros and Cons

Options are limited when faced with overwhelming debt, making Chase debt settlement an attractive choice. While it offers potential benefits, understanding the risks is critical before you take the plunge.

Benefits of Chase Debt Settlement

Firstly, debt settlement allows you to potentially settle your debt for less than the full amount owed. This can provide substantial savings and help you get out of debt faster. Secondly, it can simplify your finances by consolidating multiple debts into a single payment.

Risks of Chase Debt Settlement

On the flip side, debt settlement comes with potential risks. One significant concern is the impact on your credit score. Settling your debt for less than the full amount can negatively affect your score, making it harder to obtain future credit and qualify for favorable interest rates.

Immediate Impact on Your Credit

It’s also crucial to consider the immediate consequences of debt settlement. When you enter into a debt settlement agreement, Chase will likely report your account as “settled” to the credit bureaus. This can lower your credit score and stay on your credit report for up to seven years.

Long-Term Credit Implications

Furthermore, debt settlement can have lasting implications for your credit. Lenders may view your payment history as less favorable, making it harder to qualify for loans or other forms of credit in the future. It’s important to weigh the potential benefits and risks carefully to make an informed decision that aligns with your financial goals.

Chase Debt Settlement: A Comprehensive Overview and Alternative Solutions

Debt settlement, offered by Chase and other financial institutions, can be a viable option for those struggling to repay their debts. However, it’s essential to consider the potential ramifications and explore alternative solutions before making a decision. In this comprehensive guide, we’ll delve into the intricacies of Chase debt settlement and provide you with a detailed examination of alternative strategies for managing your debts.

Understanding Chase Debt Settlement

Chase debt settlement involves negotiating with creditors to reduce the amount of money you owe. Typically, you’ll make a lump-sum payment to settle the debt, which is often less than the original balance. While debt settlement can provide a way out of overwhelming debt, it’s important to be aware of its potential drawbacks, such as negative impacts on your credit score and tax implications.

Alternatives to Chase Debt Settlement

If debt settlement isn’t the right path for you, there are various other ways to manage your debts. Let’s delve deeper into some effective alternatives:

Debt Consolidation

Debt consolidation is a process where you combine multiple debts into a single, more manageable loan. This can be beneficial if you have high-interest debts and want to lower your monthly payments. There are various options for debt consolidation, such as balance transfer credit cards, personal loans, and home equity loans.

Debt Management Plan (DMP)

A debt management plan is a program offered by non-profit credit counseling agencies. It involves working with a counselor to create a personalized plan for repaying your debts. DMPs often include reduced interest rates, lower monthly payments, and protection from creditors.

Consumer Credit Counseling

Consumer credit counseling is another option available through non-profit agencies. Counselors can provide guidance on budgeting, debt management, and other financial matters. They can also assist with negotiating with creditors and creating realistic repayment plans.

Balance Transfer Credit Card

A balance transfer credit card allows you to transfer high-interest debts to a card with a lower interest rate. This can be a cost-effective way to reduce the amount of interest you pay on your debt. However, it’s crucial to consider any balance transfer fees or introductory interest rates that may apply.

Home Equity Loan or Line of Credit

If you have equity in your home, you may be able to use a home equity loan or line of credit to consolidate your debts. This can be a good option if you have a good credit score and can qualify for a low interest rate. However, it’s important to remember that you’re using your home as collateral, so defaulting on the loan could result in foreclosure.

Managing debt can be challenging, but it’s crucial to explore all available options and seek professional advice if needed. By weighing the pros and cons of Chase debt settlement and considering the alternatives, you can make an informed decision that fits your unique financial situation.

No responses yet