Credit Consolidation vs Debt Settlement: Which Option is Right for You?

When faced with overwhelming debt, it can be tough to know where to turn. Two popular options are credit consolidation and debt settlement. But what’s the difference between the two, and which one is right for you?

Credit Consolidation

Credit consolidation involves combining multiple debts into a single loan, typically with a lower interest rate. This can make it easier to manage and pay off debt, as you’ll have just one monthly payment to worry about. There are two main types of credit consolidation loans:

- Balance transfer credit cards: These cards allow you to transfer your existing debt from multiple cards onto a single card with a lower interest rate.

- Personal loans: These loans can be used to consolidate debt from various sources, such as credit cards, medical bills, and payday loans.

Pros and Cons of Credit Consolidation

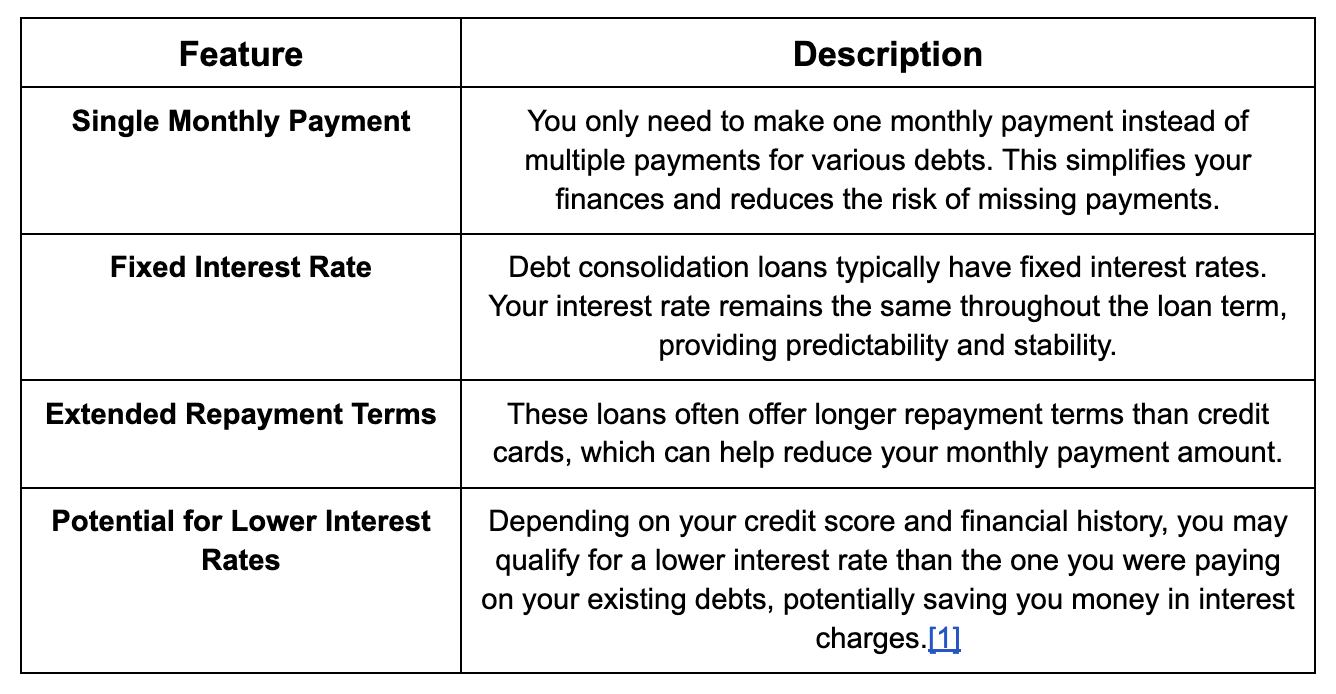

Pros:

- Lower interest rates

- Simplified monthly payments

- Improved credit score (if payments are made on time)

Cons:

- May not be approved for a loan

- May be subject to fees

- May increase your total debt if the loan has a longer term

Debt Settlement

Debt settlement is a process in which you negotiate with your creditors to pay off your debts for less than the full amount. This can be a good option if you’re unable to make your current debt payments. However, it’s important to note that debt settlement can have negative consequences, such as:

- Damage to your credit score

- Tax liability on the forgiven debt

- Difficulty obtaining credit in the future

Pros and Cons of Debt Settlement

Pros:

- Can significantly reduce your debt

- Can eliminate the need for monthly payments

Cons:

- Can damage your credit score

- May be taxed on the forgiven debt

- Can be difficult to obtain credit in the future

Which Option is Right for You?

The best option for you depends on your individual circumstances. If you have good credit and can qualify for a low-interest credit consolidation loan, this may be a good option for you. However, if you’re unable to make your current debt payments, debt settlement may be a better choice.

Conclusion

Credit consolidation and debt settlement are both viable options for dealing with debt. The best option for you depends on your individual circumstances. It’s important to weigh the pros and cons of each option before making a decision.

Credit Consolidation vs. Debt Settlement: Which One Is Right for You?

If you’re struggling with overwhelming debt, you may be considering credit consolidation or debt settlement. Both options can help you manage your debt more effectively, but they have different pros and cons. Let’s dive into the details to help you determine the best solution for your financial situation.

Credit Consolidation: A Traditional Solution

Credit consolidation involves taking out a new loan (typically a personal loan or balance transfer credit card) to pay off your existing debt. This can simplify your debt repayment process and potentially lower your interest rates. Consolidating your debt can also improve your credit score if you make your payments on time. However, keep in mind that you may still have to pay additional fees associated with consolidation loans.

Debt Settlement: A Last Resort Option

Debt settlement is a more drastic measure that involves negotiating with your creditors to pay back less than the full amount owed. While this option can provide quick debt relief, it does come with some serious risks and consequences. Debt settlement can damage your credit score significantly and make it difficult to obtain future loans. Additionally, you may be required to pay taxes on the amount of debt that is forgiven.

Key Points to Consider When Choosing Between Credit Consolidation and Debt Settlement

- Can you afford the monthly payments? Credit consolidation can lower your monthly payments, but you need to make sure you can afford them.

- What is your credit score? Credit consolidation can improve your credit score, but debt settlement can damage it.

- What are your long-term goals? Credit consolidation can help you get out of debt faster, but debt settlement can provide quick relief if you need it right away.

Which One Is Right for You?

The best option for you will depend on your individual circumstances. If you have good credit and can afford the monthly payments, credit consolidation is a good choice. If you have bad credit or need immediate relief from your debt, debt settlement may be your only option. However, proceed with caution and be aware of the potential risks.

Ultimately, the decision between credit consolidation and debt settlement is a personal one. By weighing the pros and cons carefully and considering your individual needs, you can make the best choice for your financial future.

Credit Consolidation vs. Debt Settlement: Which is Right for You?

If you’re drowning in debt, you may be wondering whether credit consolidation or debt settlement is the right way to dig yourself out of the hole. Both options can have their pros and cons, so it’s important to weigh the benefits of each before making a decision.

Credit consolidation involves taking out a new loan to pay off your existing debts. This can help you to simplify your payments and potentially reduce your interest rate. However, it’s important to note that credit consolidation will not reduce the total amount of debt you owe. Furthermore, if you have bad credit, you may not be able to qualify for a credit consolidation loan with a favorable interest rate.

Debt settlement, on the other hand, involves negotiating with your creditors to pay less than the full amount you owe. This can be a good option if you’re struggling to make your monthly payments and you have a low income. However, debt settlement can damage your credit score and make it difficult to qualify for loans in the future.

Choosing Between Credit Consolidation and Debt Settlement

The best option for you depends on your financial situation and goals. Credit consolidation may be a good option if you have good credit, a stable income, and you’re confident that you can make your monthly payments on time. Debt settlement may be a better option if you’re struggling to make your monthly payments, have a low income, and you’re willing to accept the potential damage to your credit score.

Credit Consolidation vs. Debt Settlement: Which Option Is Right for You?

When it comes to managing overwhelming debt, individuals often grapple between two primary strategies: credit consolidation and debt settlement. Each approach possesses its own set of advantages and drawbacks, and the optimal choice hinges upon one’s financial situation and long-term goals.

Credit Consolidation: Pros and Cons

Pros:

- Lower interest rates: Credit consolidation loans typically offer lower interest rates than credit cards, reducing the overall cost of borrowing. This can result in substantial savings over time.

- Simplified payments: Consolidate your debt into a single monthly payment, simplifying your debt management and reducing the risk of missed payments.

- Potential for credit score improvement: Making consistent payments on time can positively impact your credit score, improving your future borrowing prospects.

Cons:

- May require a good credit score: Lenders often require applicants to have a good credit score to qualify for consolidation loans. If your credit score is low, you may be denied or offered unfavorable terms.

- Could limit future borrowing: Taking out a consolidation loan can reduce your available credit, potentially limiting your ability to borrow additional funds in the future.

- May not reduce total debt: Credit consolidation does not reduce your total debt balance. It simply combines your debts into a single loan, potentially extending the repayment period and increasing the total interest paid over time.

Debt Settlement: Pros and Cons

Pros:

- Potential for significant debt reduction: Debt settlement can potentially reduce your outstanding debt balance by a substantial amount, providing immediate relief from financial stress.

- Avoids long-term debt repayment: Unlike consolidation, debt settlement allows you to pay off your debts quickly, freeing you from the burden of long-term repayment plans.

- Credit score does not play a role: Your credit score does not typically impact your eligibility for debt settlement. This can be an advantage for individuals with poor credit.

Cons:

- Can damage your credit score: Debt settlement involves negotiating with creditors to reduce your debt balance, which can negatively impact your credit score.

- Can take time: The debt settlement process can be lengthy, taking up to several years in some cases.

- Fees and expenses: Debt settlement companies often charge fees for their services, which can further increase the total cost of resolving your debt.

Credit Consolidation vs. Debt Settlement: Which Is Right for You?

If you’re drowning in debt, it’s easy to feel like you’re up a creek without a paddle. But fear not, my friend! There are two life rafts that can help you navigate the treacherous waters of financial distress: credit consolidation and debt settlement. Both options offer unique advantages and drawbacks, so it’s crucial to weigh them carefully before taking the plunge.

Pros and Cons of Debt Consolidation

Pros:

- Lower interest rates: By consolidating multiple debts into a single loan, you can secure a lower interest rate, which can save you a bundle of dough over time.

- Easier payment plan: Instead of juggling multiple payments, you can simplify your life with one monthly payment.

- Improved credit score: On-time payments can gradually improve your credit score, opening the door to better financial opportunities down the road.

Cons:

- High fees: Some consolidation companies charge hefty fees for their services, so be sure to shop around and do your research.

- Not always suitable for large amounts of debt: If you’ve got a mountain of debt, consolidation may not be the best option for you.

- Can lead to new debt: It’s possible to fall into the trap of taking on more debt to consolidate your existing debt, so proceed with caution.

Pros and Cons of Debt Settlement

Pros:

- Significant debt reduction: Debt settlement programs can negotiate a hefty reduction in your overall debt, giving you much-needed breathing room.

- Quick debt relief: Compared to consolidation, debt settlement can provide faster relief from your financial worries.

Cons:

- Damages credit score: Debt settlement deals a major blow to your credit score, making it difficult to secure loans or other forms of credit in the future.

- May face tax consequences: The forgiven debt may be considered taxable income, so be prepared to pay additional taxes.

- Could harm relationships with creditors: Debt settlement can strain your relationships with the creditors you’re negotiating with.

Which Option Is Right for You?

The best option for you depends on your specific financial situation. If you have a good credit score, a manageable amount of debt, and you’re prepared to pay consolidation fees, then credit consolidation may be a wise choice. On the other hand, if you’re facing an overwhelming amount of debt, you’re willing to accept the consequences of a damaged credit score, and you prioritize quick debt relief, then debt settlement could be a viable option.

Ultimately, the decision of whether to consolidate or settle your debt is a personal one. By carefully considering the pros and cons of each option, you can choose the path that leads to financial freedom and peace of mind.

Credit Consolidation vs. Debt Settlement: Unpacking Your Options

In the labyrinth of debt management, individuals often find themselves torn between credit consolidation and debt settlement. Understanding the nuances of each option is crucial for making an informed decision that aligns with your financial goals.

Credit consolidation, like a financial jigsaw puzzle, merges multiple debts into a single loan with a lower interest rate. This can streamline payments, potentially reducing monthly expenses. Debt settlement, on the other hand, involves negotiating a lump-sum payment with creditors, typically for less than the total amount owed. This can expedite debt repayment, but it may damage your credit score.

When to Consider Legal Help

If the weight of debt is crushing you, seeking legal assistance is a prudent course of action. A bankruptcy attorney can provide expert guidance, ensuring that your rights are protected and that you’re exploring all available options.

Bankruptcy is often the last resort when all other avenues have been exhausted. However, it’s important to weigh the potential consequences, such as the impact on credit scores and future borrowing ability. Consulting an attorney can help you make an informed decision about whether bankruptcy is the right path for you

Understanding the Pros and Cons

Credit Consolidation:

- Can lower interest rates and simplify payments

- May require qualifying for a new loan

- Can be costly, especially if fees are high

Debt Settlement:

- Can result in significant debt reduction

- Can damage credit scores

- May require upfront fees or payments

Choosing the Right Option for You

The choice between credit consolidation and debt settlement depends on your unique financial situation. If you have a steady income and good credit, credit consolidation may be a viable option. However, if your debt is overwhelming and your credit is damaged, debt settlement might be a more suitable solution.

Before making a decision, consider your long-term financial goals. If you’re planning on making large purchases or applying for loans in the future, credit consolidation may be a better choice. If you simply want to get out of debt as quickly as possible, debt settlement may be the way to go.

Seek Professional Guidance

Navigating the complex world of debt management can be daunting. Seeking professional guidance from a bankruptcy attorney or credit counselor can provide you with the clarity and support you need to make an informed decision. They can assess your situation, explain your options, and help you develop a personalized plan to overcome your debt challenges.

No responses yet